- Aid Packages: Breaking Them Down

- High School Juniors: The Golden Opportunity

- Financial Aid Insider: Students Get Help Why Not Parents?

Date: February, 2020

Dear Parent,

|

February is the second month of the year in the Julian and Gregorian calendars, with 28 days in common years and 29 days in leap years like this one, with the quadrennial 29th day being called the leap day. It is the first of five months to have fewer than 31 days (the other four being April, June, September, and November) and the only one to have fewer than 30 days. The other seven months have 31 days. |

Breaking It All Down

We see acceptances and the aid packages coming in now. Some colleges have been more forthright in explaining what the award letters actually mean, but some have not.

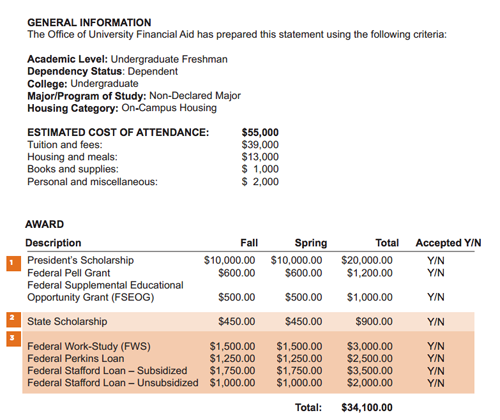

What you want to see is something that looks like the sample letter below. The package should include the estimated cost of attendance -- which includes tuition and fees, housing and meal plans, books, supplies, personal or miscellaneous expenses. And although not included in the example, a travel allowance should also be included.

The Nitty Gritty

|

The awards themselves are not typically explained in detail, so here's some help. In this case, the package is broken into four sections. First, the college shows its list price. Second are scholarships and grants awarded by the college. The third is a merit scholarship given by the student's state of residence. The fourth are student loans and work-study. This is considered self-help. About awards. Their meanings are not always clear. Some scholarships are based on merit, while others are really grants based on financial need. As long as your student maintains the required minimum GPA and is a student in good standing, the dollar amount of merit awards shouldn't. |

Most grants are labeled as such. The dollar amount is usually variable based on annual changes of income and assets. If the student receives a scholarship, and there is still a good deal of eligibility for more aid and isn't offered a grant, it probably means one of two things: they don't have the money in their budget OR they don't have the money for your student.

In the fourth section, Federal Work-Study. FWS is an on-campus job BUT it's not guaranteed. Your student has to apply for it just like any other. In fact, there are more offers of FWS than there are actual jobs so applicants must be aware of application procedures and deadlines or risk losing out.

|

Lastly, student loans. Federal loan amounts for first-year undergraduate students are in most cases limited to $5,500. They may be broken into two types depending on your family's need and cost of attendance. These are subsidized and unsubsidized. There are no credit or background checks, and no co-signers required. This loan will be the student's responsibility. For subsidized loans, interest will be paid by the government as long as the student remains in school at least half-time, and for six months after finishing. For unsubsidized loans, interest will accrue over the course of the student's college years. The interest is compounded-- added back into the loan each year. This means that the student will be paying interest on interest. |

|

If the award letter doesn't include indirect expenses, I suggest you contact the college and ask what they estimate those costs to be. This may give you some leverage when you go to negotiate. Or you could go to the College Board website and look them up in the Paying section.

About Your High School Junior: Golden Opportunities

|

Last February, I wrote about Test-Optional colleges. However, given the fast-changing admissions landscape and the cost of four-year schools, I think it more important for now that you really understand what the colleges are going through right now, and how you can benefit. Competition is still fierce at the brand name colleges, like the Ivies, USC, Rice, Duke, UCLA, and the like. But according to the National Student Clearinghouse Research Center, since 2011, enrollment has decreased by almost three million students. |

In fact, according to the bond rating company Moody's, since 2016, 33 colleges have closed their Ivy Halls due to falling enrollments. So, what's that got to do with the price of beans? Plenty! Especially when last year more than 400 colleges and universities still had seats available for freshmen and transfer students after the traditional May 1st deadline to enroll for this past Fall, as reported by the National Association for College Admission Counseling.

In 2018, only 38% of four-year colleges filled all of their seats. This represents a golden opportunity to drastically reduce out of pocket college costs! After all, colleges are businesses, and they need to keep the lights on. Think of it like this: you can usually get a better deal on a car at the end of the month. That's so dealers can meet their quotas and get the cars off their lots. Come May or June 1st, admissions at many fine colleges are frantic to meet their quota, and if they have to discount tuition to do it, they will.

There are colleges that are combining with other institutions. This can be a good thing. Just as private companies might do to increase their size and cost-effectiveness.

|

Some colleges are doing things that benefit students directly by offering money-saving accelerated programs, through which students can get both undergraduate and graduate degrees more quickly than it would take them elsewhere, such as a five-year combined B.A. and M.B.A. |

|

Others are figuring out how to increase the number of credits each semester a student can take and also picking up credits over winter break, so students can graduate in three years.

Colleges like Davenport University offer graduates who can't find jobs in their majors an additional 48 credits to help them advance their degrees. The only proviso is that the job guarantee applies only to majors in the highest demand fields.

There are many ways a student can get a reasonably priced and faster college education from an established institution, including community college, online classes, dual enrollment-- not to mention AP classes.

|

|

Before a college gives their own money to your student, the more selective institutions are requiring more financial information each year. Some colleges are asking you to list the balances in your bank and brokerage accounts! Who knows? Someday they might insist on knowing your account numbers, usernames and passwords to verify your assets.

While the Free Application For Federal Student Aid or FAFSA hasn’t gone that far yet, the colleges are free to ask anything they want. The College Board’s Financial Aid Profile has added on average eight new questions each year, making the shortest form 13 pages long… not including dependent verification statements, tax returns, W-2s, 1099’s, non-tax filing forms, business returns, or the worst of all possible forms for the business owner: the Business/Farm Supplement.

There are about a dozen more forms a college could ask you to complete.

More questions and more forms multiply your chances of making costly errors. Those parents who are busy, divorced or separated, have had significant changes in their family and finances, or are business owners with students applying to selective colleges I encourage you to get the advice of a financial aid professional. They save you money, time, and frustration.

One last thing, because this years financial aid award is based on your 2018 Federal Tax return, if you made substantially less money in 2019 or expect to in 2020, I recommend that make an appeal to the college to consider your changed situation. Your financial aid professional can help you with this.

Well, that's it for this month.

Your College Cruise Director,

Stuart Phillip Siegel,

Founder, College Tuition Solutions, Inc.

Creator of College for Pennies and

FAFSAsoft Financial Aid Management Software for the Professional College Advisor

208-639-1330

|

|

PS The next time you're with a friend with college-bound children, please tell them about us and share this email with them. As you know college is becoming unaffordable to far too many families. Anything we can do to help them I’m certain they will be highly appreciative.

Copyright © 2012-20 CTS, Inc. All rights reserved.